We feel that this scheme was rolled out too hastily and falls remarkably short of its purported priority of providing secure and stable long-term homeownership to aspiring first-time homeowners.

While the prospect of moving into a, say, RM250,000 house – for five years – instantly with only a downpayment of RM50,000 (or 20%) might seem alluring at first glance, we are fearful that first-time homeowners may be obscured from the scheme’s long-term implications.

First-time homeowners intending to stay for over 5 years will be worse off

For a start, buyers do not have full ownership of the property, and their rights as an owner are only fully realised once they have fully paid for the property after the initial five-year period.

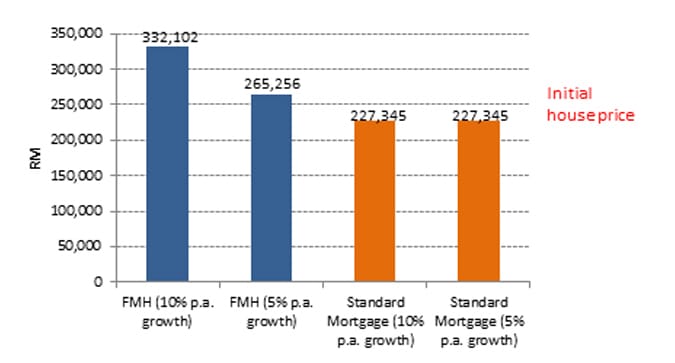

According to our calculations, first-time homeowners intending to stay in the property for more than five years will be financially worse-off by the end of Year 5 (Figure 1).

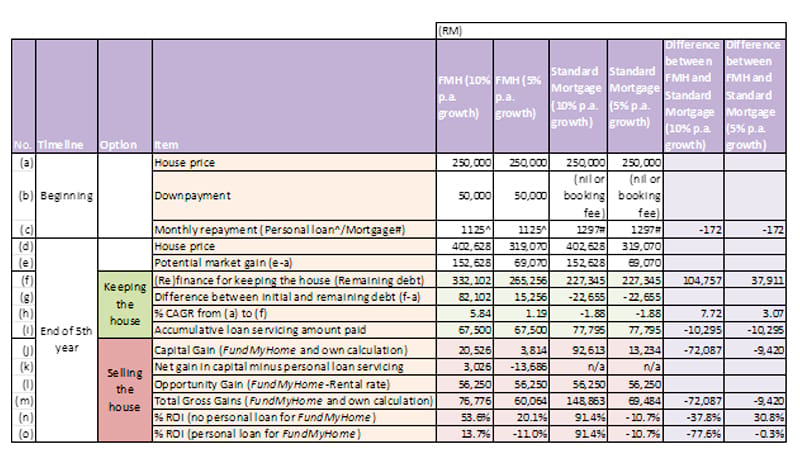

Row (f) of Table 1 and Figure 1 show that if the annual home value appreciation rate is 5% per annum, buyers would end up with an additional debt of RM37,911 relative to a scenario where they utilised a standard mortgage.

This additional debt figure rises to a staggering RM104,757, relative to a standard mortgage if the annual home value appreciation rate is 10% per annum.

This shows unequivocally that the price of refinancing – necessary to keep the house beyond the initial five-year period – is much higher than that of a standard mortgaged property.

Buyers will need their household income to increase by at least 5.81%, or 1.19% in compound annual growth rate (CAGR), during the five years just to keep pace with the burgeoning home value.

If a first-time homeowner is not able to afford a standard mortgage for the said property at the beginning, it is highly unlikely he or she will be able to afford a significantly higher refinancing cost five years later (see Rows (f) and (g) of Table 1).

Few lower-middle-income households are likely to have a reserve outlay at the scale of RM50,000 to pay upfront as investment funds, assuming a RM250,000 property price.

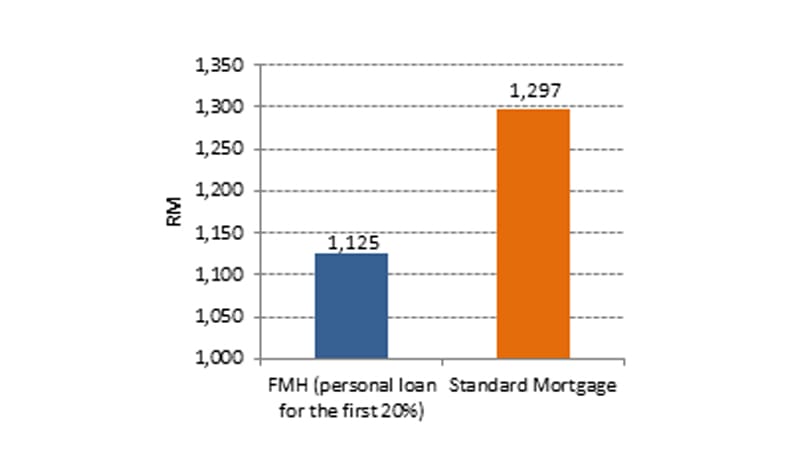

Should buyers raise funds through personal loans to pay the initial 20% (RM50,000), their monthly repayment will be roughly RM1,125, which is just RM172 less than that which is required from a standard mortgage repayment scheme (Figure 2).

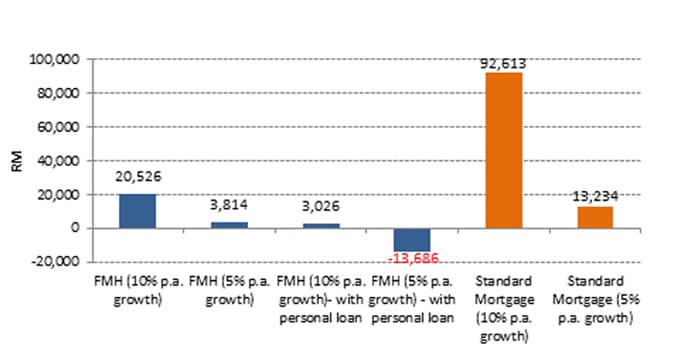

By the end of the stipulated fifth year, buyers would have already paid RM67,000 for the personal loan and should buyers chose to “sell” the property – assuming a 10% annual appreciation rate – FundMyHome claims that they will make total gross gains of RM76,776 (inclusive of the RM20,526 in capital gains and RM56,250 rental opportunity gains).

If the buyer were to stay during the first five years, however, these rental opportunity gains would not materialise. By subtracting the cost of the personal loan from a buyer’s capital gain, he or she would be left with a paltry net gain of RM3,026 after five years of this scheme (assuming home value appreciation of 10% annually) (Figure 3).

Cumulatively, the cost of a standard mortgage is undeniably higher in this case (as Row (i) indicates, an additional RM10,295 after 5 years), but the mortgage offers ownership of longer than five years, and the buyers may potentially retain all the property’s future capital gains.

In this sense, the majority of the benefits of the FundMyHome programme accrue only if a “buyer” is seeking a short-term (five-year) rental agreement, and not if they are seeking to become a first-time homeowner.

The enormous contradicting factor here, though, is that the FundMyHome scheme is itself marketed as one which assists consumers in becoming homeowners.

No guarantee of an average annual home appreciation of 10%

Also, there is no guarantee of an average annual home appreciation of 10% over five years; FundMyHome has stated that the price of any property may go up or down. If the price of a property goes down, the buyer stands to lose some or all of his capital.

The potential earnings that the FundMyHome has been promoting arguably rests on an overly optimistic view of a healthy economic and housing boom – one which nobody can confidently predict that will even come to fruition.

Even if this was the case, wouldn’t it be better for a prospective homeowner to go for a standard mortgage which can gain about a 38% (or RM72,087) return on investment (ROI) in addition (see Rows (m) and (n) of Table 1)?

Furthermore, the scheme’s small print indicates that the investor will always receive a preferential share of the capital gain (equivalent to 20% of purchase price) if the property value increases, while the remaining capital gain would only subsequently be split proportionately (20% to the buyer, 80% to the investor) after the sale in the fifth year.

In short, buyers require a property’s value to rise by 20% in order for them to make any financial gains in addition to their initial 20% upfront payment.

If the housing market experiences a downward slump of at least 20%, the buyer stands to lose every ringgit of his or her “investment”. This makes us question strongly whether the whole purpose of this FundMyHome scheme is really to ease the burden of first-time homeowners, or whether it is just another form of investment scheme?

Other questions that need to be answered

There are some other questions which need to be raised before the scheme is fully implemented. What if a large majority of Malaysian participants are unable to afford the house after five years and are forced to vacate the premises?

Wouldn’t such practices shock and crash the housing market due to the scheme’s creation of cyclically large surpluses of vacated properties? Would this lead to the creation of a housing bubble which renders the task of first-time homeownership far more difficult and financially taxing?

Secondly, has the public been informed about the higher cost of refinancing a property under FundMyHome after five years as opposed to a standard mortgage loan? First-time homeowners need to be able to at least compare and contrast the differences between standard mortgage loans and FundMyHome in order to make an informed and responsible investment decision.

We are of the view that the government should be wary of this new housing scheme, as analysis and calculation shows that it does not benefit first-time homeowners in any sense but rather resembles an inferior investment scheme that hedges on future property values.

It is a responsibility of the government to ensure housing affordability to the rakyat through truly beneficial schemes and initiatives, instead of just helping developers solve their property overhang issues – which exist only because of developers’ stubborn unwillingness to adjust their inflated property prices downwards.

In the end, the claim that this scheme is to the benefit of the rakyat is a gross exaggeration – it is the developers and vaguely-defined “institutional investors” that will benefit from FundMyHome.

The scheme is bad news for Malaysians.

Agora Society Malaysia is a loose network of individuals who believe in the principles of democracy and good governance.

The views expressed are those of the authors and do not necessarily reflect those of FMT.