Their analysts have held firm on their calls for IHH, expecting patient throughput to improve in both the domestic and international markets.

Net profit for the fourth quarter came in at RM191.7 million, a 58% decrease from the same quarter last year, and 23.8% lower than the preceding quarter at RM251.7 million.

Group CEO Joe Sim said the group recorded a robust core performance with revenue growth amidst inflationary pressures, rising interest rates and a sharp drop in Covid-19-related services.

“Reported net income was mainly impacted by a one-off RM305.9 million impairment in China which will better position us for the year ahead, as well as higher operating costs,” he said.

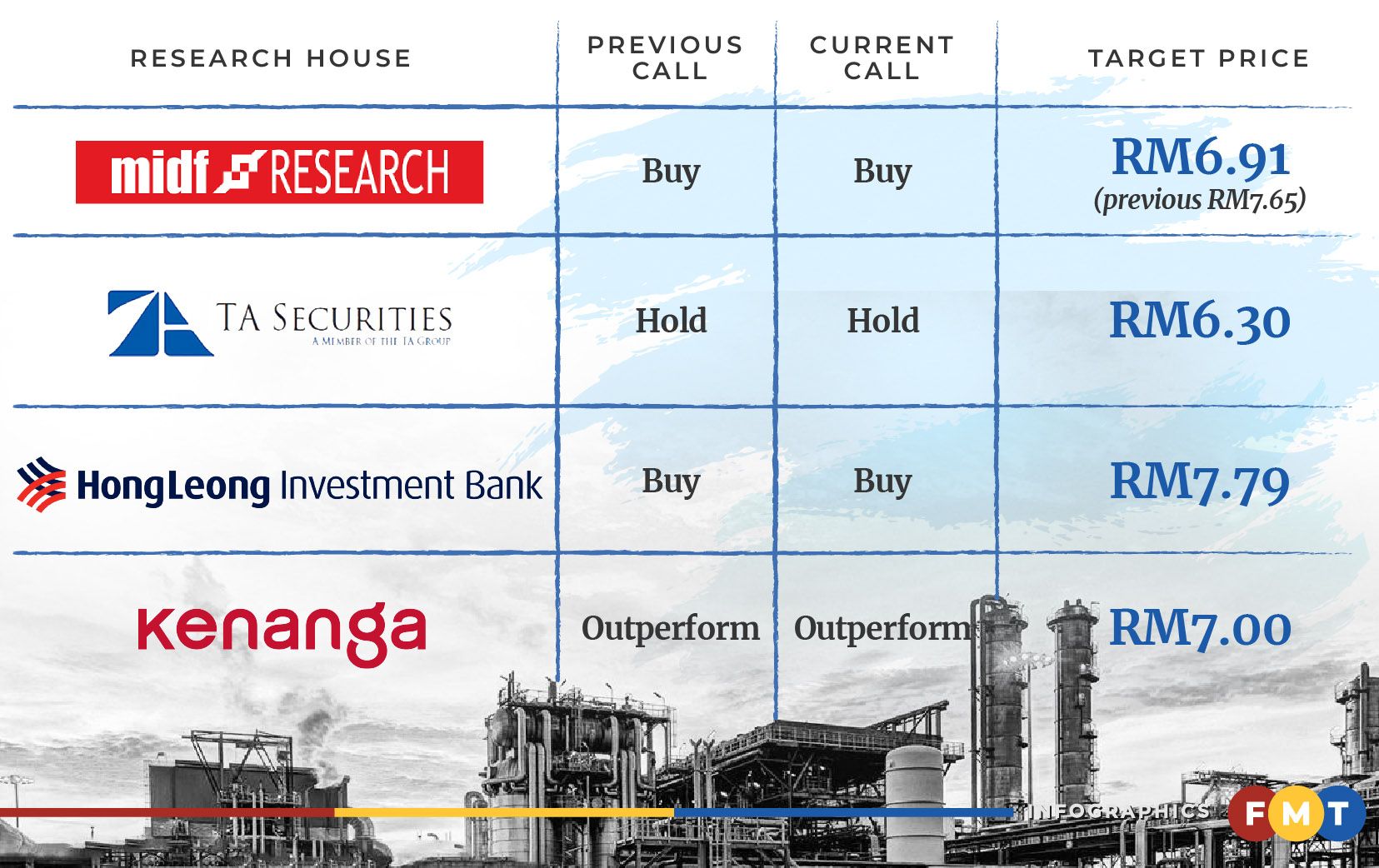

Kenanga Research has retained its ‘outperform’ call on IHH, and their target price (TP) of RM7.

“The group expects double-digit growth in 2023 (which we have factored into our forecast), driven by sustained pent-up demand for elective surgeries, from both local and foreign patients,” said Kenanga.

Despite expectations that the healthcare industry will continue to face increasing costs due to inflation, high energy prices and nursing shortages, Kenanga does not foresee large impact on IHH.

“The group is unperturbed by any potential slowdown in demand. This is because IHH caters to a particular segment which is less price sensitive (allowing it to) pass on cost inflation to customers, as reflected in its rising revenue per inpatient over the past several quarters,” it said.

Similarly, MIDF Research has maintained its ‘buy’ call with a TP lowered to RM6.91 from RM7.65.

“Despite our optimism regarding IHH’s prospects in FY2023, we believe that the global inflation and rising interest rates, IHH’s China assets, as well as shortages in medical equipment and staff, will continue to have a significant impact on the group’s operating costs,” it said.

Hong Leong Investment Bank (HLIB) Research said cost pressures will ease in FY2023, mainly on lower electricity and labour costs, and has maintained its “buy’’ call with a TP of RM7.79.

It also likes IHH for its potential to grow further via both organic and inorganic means, as well as its strong market position in all key markets that it operates in.

Similarly, TA Research reiterated its “hold’’ on IHH with an unchanged TP of RM6.30 a share.

Focused on growth

For the year ahead, IHH shared that the group’s focus on growth would see it emphasising return on equity and acquiring strategic assets, it said in its Bursa Malaysia filing recently.

“The group is cautiously optimistic of robust growth from its core business with the return of local and foreign patients to its hospitals,” it said.

“The group’s hospitals in Turkey were unscathed by the recent earthquake in the region, and have stepped up to provide medical support to quake victims across the country.”

This year, the group expects to complete the sale of IMU Group (its education business in Malaysia). Additionally, the divestment of Gleneagles Chengdu Hospital Company Ltd, a 49%-owned subsidiary, was just completed on Feb 27.

“The sale is in line with IHH’s strategy to continually review its asset portfolio in China to minimise losses,” it added.